Buying a home is one of life’s most meaningful financial milestones. For most homeowners, a home loan becomes an inevitable part of that journey – a long-term commitment that runs quietly in the background of everyday life. Over time, as careers progress and savings grow, many homeowners find themselves at a familiar crossroads: should surplus money be used to prepay the home loan, or is it wiser to invest that amount elsewhere?

A year-end bonus, a salary hike, a maturing investment, or even disciplined savings can bring this question to the forefront. While both choices have merit, the answer is rarely universal. Understanding how each option works – financially and practically – is essential before making a decision.

Understanding What Home Loan Prepayment Really Offers

Prepaying a home loan essentially means paying an additional amount over and above your regular EMIs, directly toward the principal. Since interest is calculated on the outstanding principal, reducing this amount leads to lower overall interest outgo.

1. Interest Savings Over Time

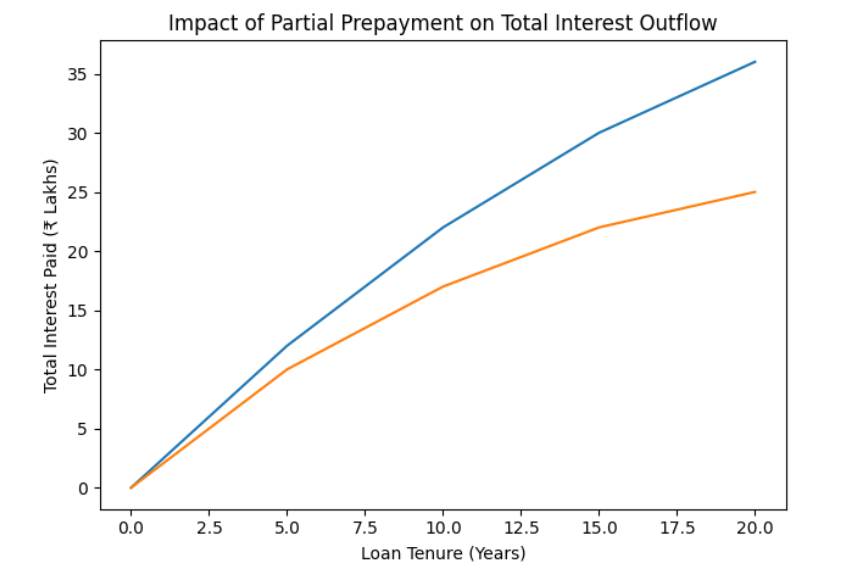

The most direct benefit of prepayment is the reduction in interest paid across the loan tenure. Even a partial prepayment early in the loan cycle can result in significant savings, as interest payments are highest during the initial years.

Line graph showing total interest paid over time — with and without partial prepayment.

Borrowers usually have two choices after prepayment:

- Reduce the loan tenure while keeping EMIs constant

- Reduce the EMI amount while keeping tenure unchanged

For most salaried individuals, maintaining the EMI and shortening the tenure often results in better interest savings.

2. Predictability and Financial Comfort

Beyond numbers, prepayment offers a sense of certainty. A lower outstanding loan reduces long-term obligations and can free up future income for other goals. For individuals who value financial stability and lower monthly liabilities, this aspect carries weight.

The Investment Alternative: Letting Money Work Elsewhere

Instead of prepaying, surplus funds can be invested in instruments such as equity mutual funds, fixed-income products, or a mix of both. The logic here is simple: if investments can generate returns higher than the effective home loan interest rate, investing may prove more beneficial in the long run.

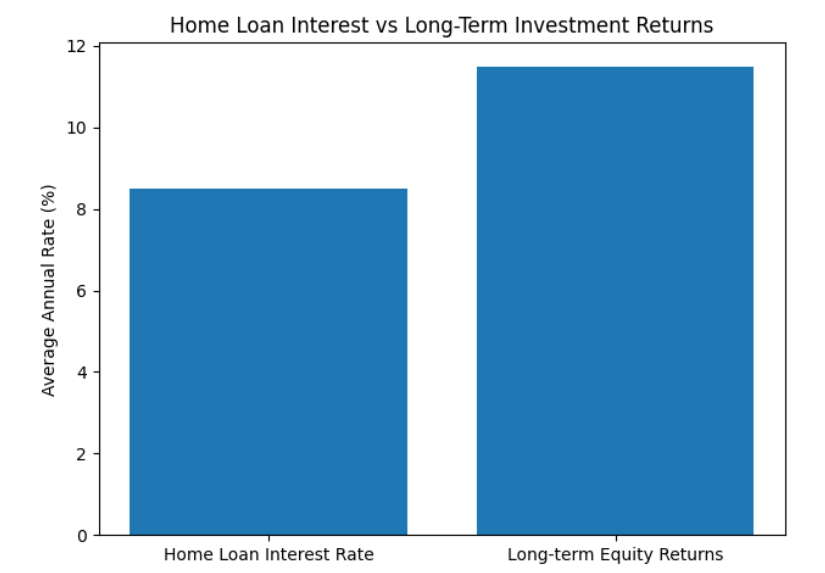

3. Comparing Returns and Loan Costs

Home loan interest rates typically range between 8–9% per annum. Long-term equity investments, while market-linked, have historically delivered average returns in the 10–12% range over extended periods.

Bar chart comparing average home loan interest rates vs long-term equity investment returns.

This difference, when compounded over time, can be substantial – provided the investor is comfortable with market fluctuations and stays invested long enough.

4. Liquidity and Flexibility

Investing surplus money retains liquidity. Unlike loan prepayment, invested funds can be accessed during emergencies or redirected toward other life goals. This flexibility is often a deciding factor for younger homeowners or those with evolving financial responsibilities.

The Tax Perspective: A Factor That Cannot Be Ignored

Tax benefits play a significant role in this decision-making process.

- Section 24(b): Allows deduction of up to ₹2 lakh per year on home loan interest

- Section 80C: Offers deductions up to ₹1.5 lakh on principal repayment

- Section 80EE (eligible cases): Additional ₹50,000 deduction for first-time buyers

For many borrowers, these deductions reduce the effective cost of borrowing, making aggressive prepayment less compelling from a purely financial standpoint.

So, Which Option Makes More Sense?

There is no single answer that fits every homeowner. Prepayment works well for those who:

- Prefer certainty over potential gains

- Are closer to retirement

- Want to reduce long-term liabilities

Investing may suit those who:

- Have a longer time horizon

- Are comfortable with market-linked returns

- Want to maintain liquidity and flexibility

In many cases, a balanced approach works best – partial prepayment combined with disciplined investing – allowing homeowners to reduce interest costs while still benefiting from wealth creation.

A Thoughtful Conclusion

Home loans are long-term commitments, and decisions around them deserve patience and clarity. Whether you choose to prepay or invest, the right choice is the one that aligns with your income stability, risk tolerance, and future goals. Rather than rushing to close a loan or chasing higher returns, a measured, informed approach often delivers the most sustainable financial outcome.